What links Alameda, Gemini lending, Roger Ver, 3 arrows capital & FTX, and technically also bitconnect?

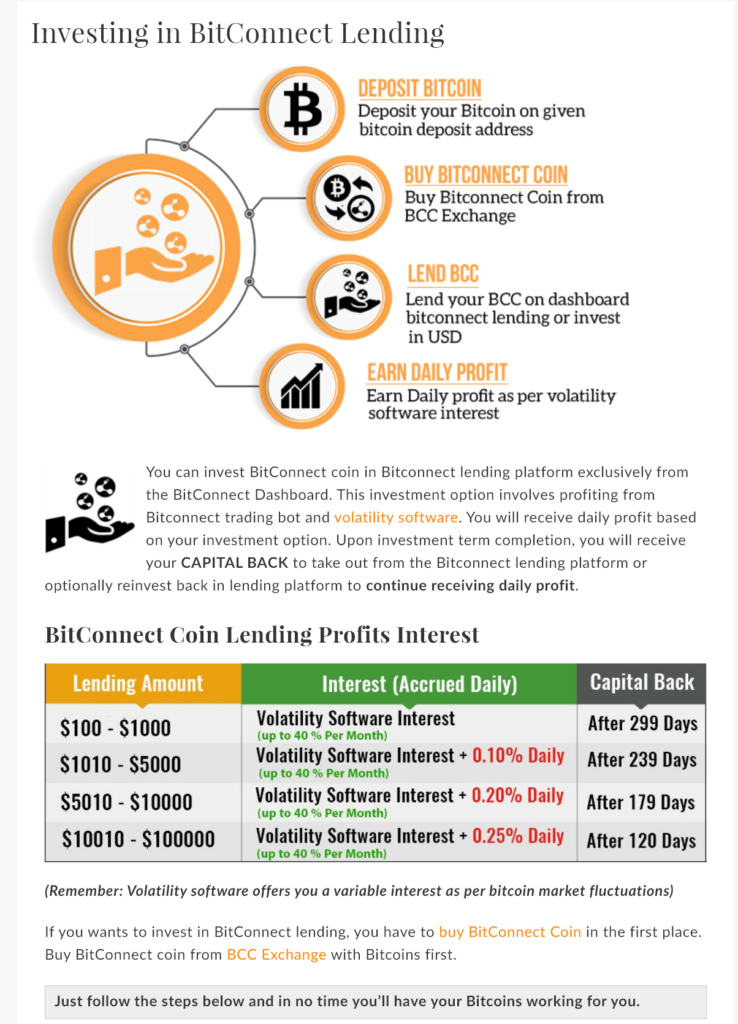

The first crypto lending platform was probably the well known ponzi scheme Bitconnect, which paid an insanely high interest rate of “1% / day” for around a year before collapsing. Bitconnect claimed that their ‘lending program’ would borrow your coins & invest them in bitconnect’s proprietary trading bot, which somehow made extreme returns off of bitcoin’s volatility.

The approach here was fairly smart, they designed the coin to use proof of stake so that the operators would get most new Bitconnect coins, which as long as capital entering the scheme would rise in value. They technically never exit scammed, instead ending the lending program, and returning all USD as Bitconnect coins at a value of $366 / coin (now worth less than $1).

A few bitconnect copycats (IE davor coin) launched in the months ahead, but people had generally realized these so called HYIP schemes were fraudulent and moved on.

Context

Before getting into a discussion on modern lending schemes, it’s worth acknowledging most inflows occurred during an unprecedented period of monetary policy, when the fed funds rate was 0, and it was near impossible to earn any interest.

DEFI lending was just gaining traction, initially paying out very favorable interest rates, mostly because the protocols were seen as riskier than they ended up being. I believe this optimism is part of what lead people to trust the imbeciles we’ll be discussing below.

Ditch BlockFi

I don’t care for fixed income as an investment class, especially not higher risk bonds / crypto lending, I much prefer the asymmetry of price speculation. As a result, the first time I heard about crypto lenders was in early 2021 when a website called “Ditch Blockfi” came out https://web.archive.org/web/20210312192141/http://www.ditchblockfi.com/), which called out the hidden risks being taken.

BlockFi paid a believable 6% interest rate, but the question still remains, where does the money come from? The answer was revealed to be proprietary trading firms & a huge portion was focused on one arbitrage trade.

GBTC Arbitrage

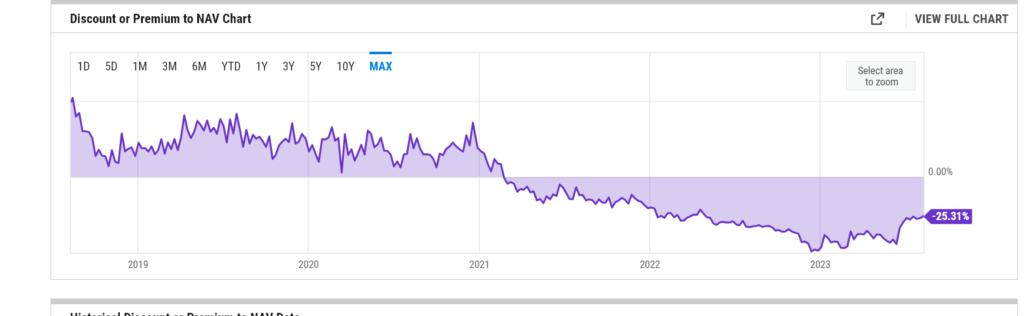

Modern GBTC discussion mostly centers around the discount, but before Feb 2021, it was the other way round. GBTC is an inelastic & fairly illiquid trading instrument, while demand for Bitcoin’s and other speculative instruments is extremely volatile (but usually rising).

The premium was self reinforcing, the fact it persisted gave investors some degree of confidence in using the GBTC vehicle to buy bitcoin. The vehicle was naturally popular for 401k account holders who wished to access Bitcoin. Given the stability of the premium, a retail investor may not have realized one existed.

GBTC has a “interesting” design, GBTC units can only be created, never redeemed for cash; new units are locked up, initially for 12 months, which was lowered to 6 months after January 2020.

Remember that Bitcoin is a very speculative & volatile asset, the demand for GBTC will fluctuate, but the supply can only ever increase. As many ‘obvious trades’ do, the dynamic changes massively when it’s played heavily.

The 2017 Bitcoin bull market never experienced a full reversion of the premium, mostly because there were few institutional players who could create GBTC units, and no ‘yield’ services. Instead the premium just fell from high to lower.

BlockFI’s bitcoin interest model was particularly well suited for this arb. GBTC would directly take Bitcoin’s to create units, which 6 months later, you could sell at the (higher) market price. Free money, and the exposure is to Bitcoins not dollars.

The lockup of coins likely contributed to the advance in the price of bitcoin heading into late 2020. The rise in Bitcoin price lead to more fomo which lead to more GBTC buying, everyone wins, until they don’t. Now the trade becomes extremely dangerous, as the ongoing bitcoin bubble masks the overload of supply.

As the premium approached 0, what appeared to be a brilliant paper profit turned into a nightmare. BlockFI & 3 arrows capital (which had borrowed from many lenders) took major losses. 3 Arrows went bust following additional bad leveraged bets on Luna, which blew up most of the weaker lenders.

(My commentary at the time).

Hidden Risk

The problem with having a concentrated loan book to high risk trading firms should be obvious to anyone aware of systemic risk. It’s also worth noting that Genesis lending is owned by the same company (DCG) as Grayscale, who operate the GBTC trust.

Diworsification

Coined by Charlie Munger to refer to diversifying into worse investments, lenders clearly made the same mistake. The critical flaw is that the main reason these firms go bust is because of risks invisible to all of them.

Firms borrowing at high interest rates are far more likely to be swimming naked.

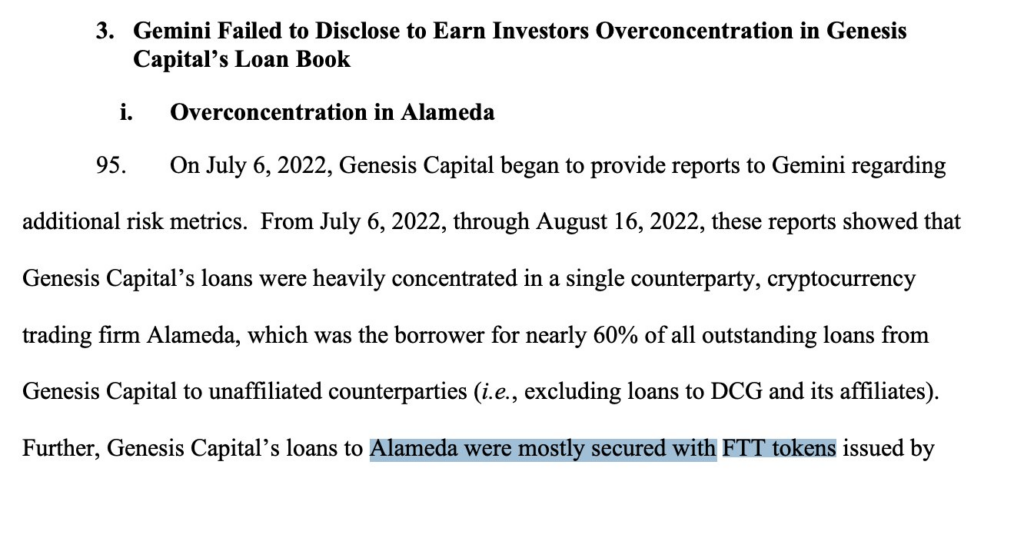

Perhaps the most foolish trade in this whole mess was lending to (secretly) insolvent trading firm Alameda Research, in exchange for FTT & SRM tokens. Any risk manager with a brain would immediately realize the problem, FTX is owned by Alameda Research, if the latter ended up in trouble, the former would also become undesirable.

Sam’s first known usage of FTT for this purpose became known during the YFI short controversy, where Sam was accused of manipulating the price of YFI down with FTT collateral. The manipulation argument is weak, but even back in 2020, Alameda (undeniably controlled by SBF at the time) was borrowing with FTT collateral, on DEFI.

Many DEFI protocols banned FTT, both from a risk management concern & also out of concern for market manipulation. Unfortunately ‘CEFI’ lenders simply fell for the SBF craze, and throughout the summer of 2022, more and more headlines started to come out about Alameda’s FTT borrowing.

Remember all the while Sam was claiming to have a billion dollar rescue fund for insolvent lenders, his real motive was clear, keep Alameda’s massive exposure from being exposed & prevent the margin call. Alameda was reliant on FTT & SRM’s prices for CEFI borrowing.

The difficulties getting funds from traditional lenders may have also motivated more aggressive utilization of customer funds. It has also been reported that all of these ‘rescue’ deals required all customer funds to be custodied on FTX, meaning that Alameda would have access to steal the funds as they wished.

Genesis & Gemini did no research

From legal proceedings related to Gemini & Genesis, most of you wouldn’t make the mistake these “experts” did. This is the same problem as Sam blaming Caroline for not hedging his illiquid investments, it’s NOT POSSIBLE.

The value of FTT as collateral is exactly 0, it’s not a collateralized loan anymore, there is no scenario where the counterparty (Alameda) is unable to pay the loan and the collateral is worth anything. It’s more akin to a convertible bond, no reasonable lender would accept common stock as collateral.

As the regulators point out, it is equally outrageous on Gemini as well, who should have immediately gone to work getting their clients money out of such a mess.

The only possible explanation besides fraud is overconfidence that Alameda was a “safe borrower”, even if the loan was horrendous. Alameda was able to against any evidence prevent a wonderkid illusion, despite most publicly known trades & investments made by the firm being flops.

CDO Squared 2.0

While some users directly lost their funds to these quasi loan sharks, others were mislead by marketing operations parroting ‘safe’ loans to reputable investment banks you’ve heard of. An example was eco, backed by prominent venture capitalists and marketing high interest rates lent to firms “like” fidelty & goldman sachs.

The reality is obviously different, these lenders were typically collecting rates of 20%+ from borrowers, that is credit card, or loan shark tier (Tonegawa of Teiai Corp pictured, Kaijii). Reputable investment banks borrow near the fed funds rate, proper collateralized loans, don’t usually trend much higher than 10%. The old saying, if you can’t see the yield in the room, you’re the yield holds true.

Unfortunately the game here is similar to CDO squared deals circa 2007, they were simply bundling other lenders such as Voyager, BlockFi & Genesis (owned by DCG) and dressing them up as legitimate. Perhaps the worst offender was FTX.us, which fraudulently claimed to be FDIC insured, until they were forced to retract that claim following a legal threat from the FDIC.

Even regulator golden boy “Gemini” exchange made the fateful decision to launch such a lending program through Genesis. Unfortunately by marketing such a risky gamble as risk free, real people get burned.

In reality, every $ invested into these platforms was also caught up in the same mess. It’s similar to the amazon scam, wherein they list cheap, awfully made sheets as “Like 1000 thread count Egyptian Cotton”, they never specified that it was, just that they were alike, perhaps in the sense they were both sheets. Loan shark debt & treasury bonds are both a form of debt, why not label them as if they were the same.

Grayscale’s GBTC fund charges fees against the NAV, not the market value. The unsustainable ballooning in GBTC’s units outstanding directly benefits Grayscale (& DCG) at the expense of retail investors, and potentially lenders.

A Look at FTX & Genesis Recent Agreement

This piece has been in the works for a while, new pieces of information kept coming out so I thought it best to hold off on finishing. One of them being the settlement between FTX & Genesis.

Whether it’s a good deal depends hugely on one’s utility function & decision system (I will cover this concept more in my upcoming risk management series). Given the generally favorable recovery available to FTX creditors, and the time value of money, I think this deal is ok.

Given the mt gox / coinlab mess, it’s probably reasonable to focus on Minimax’ing the risk of a drawn out legal battle bleeding funds & delaying payouts. The same could be said for the FTX preference claim settlement.

Conclusion

There are broad lessons to be learnt about unregulated & unsophisticated lending businesses. When investing in fixed income, I would generally recommend staying clear of any type of high yield omnibus.

If you are very confident you know what you are doing, you can do your own research, or hire an advisor / transparent fund to seek out such opportunities. Lending to opaque high yield sources will almost always result in ponzi schemes, hidden risks & ultimately severe losses.

Leave a Reply